Fin News

02/19/2020

Fin VC Navigator – 2H 2019

| Friends of Fin — We hope your 2020 is off to a tremendous start. We are reaching out to share our 2H 2019 newsletter, which we distribute publicly with the broad global ecosystem to share our perspective and thought leadership, distill Venture Capital as an asset class, promote broader participation in FinTech, and support intellectual debate. As you know, we take a long and patient view on our global relationships and as we serve as fiduciaries and add value for our entrepreneurs and partners, we recognize that growth can only come with merit. We thank our portfolio company CEOs, limited partners, co-investors, and Advisors, for your tremendous support. In these ongoing newsletters, we cover 3 areas – 1) Macro – Global/VC; 2) Micro – FinTech; and 3) Firm Updates. As always, we welcome your feedback and ideas and look forward to keeping a regular dialogue going with you all. We invite you to visit our website where we will continue to provide updates regarding firm activities, portfolio milestones, and other news and events. Feel free to e-mail us anytime at [email protected]. Our 3 asks from you:Invest with or alongside of us. We welcome new long-term limited partners as well as co-investment collaborators who are aligned with our vision for driving transformation and innovation in FinTech through early stage business formation and acceleration.Introductions to exceptional Companies and Entrepreneurs. We love to meet CEOs early and often and we welcome your ideas and introductions to companies you are bullish on!Amazing Talent. We are hiring at Fin VC and there are a number of open positions within our portfolio company network as well! We love meeting passionate and talented people and helping them find great teams and huge opportunities to work on. We are also hiring Associates and Sr. Associates in SF and NYC. See our Careers section on the website. |

| The Macro Global MacroBased on your feedback from our prior letter and the number of macro reports you all receive, we’ll keep this section succinct and link our favorite resources: As VCs, we monitor overall market conditions, but in particular cost of capital, valuations, consumer and corporate confidence, SMB support, and the overall regulatory environment for entrepreneurs, venture capital firms and the financial services industry.Overall, according to Goldman’s 2020 forecast, we will see a modest 300 bp increase in global growth to 3.4%. Despite the continued flat yield curve, recession risk remains low (20%), due in part to favorable longer-term cyclical effects, lower trade risks, continued low unemployment levels, strong household and business core financials, and the view that the US continues to represent the most attractive market for investment.The bull market has entered its 11th year, and is expected to continue, albeit with somewhat lower momentum. As always, questions linger on how much gas is left in the tank. Continued low employment suggests increasing wage pressure, and potential downward margin pressure. Geopolitical concerns remain, however the potential for improved US-China trade, reduced Brexit concerns, and improving emerging markets trends support cautious optimism. Growth in China is forecasted at 6%, representing a gradual deceleration, with some potential downside risk should the Coronavirus impact expand. That said, the global outlook remains positive, so any impact of the virus would be near-term rather than fundamental.Within the US the largest single event impact in the year will likely be the 2020 Presidential and Senate elections. All four of the leading Democratic presidential contenders (Warren, Biden, Sanders, Buttigieg) have indicated support for a partial or full repeal of the 2017 Tax Cut and Jobs Act. A repeal would return corporate tax rates from 21% to 35% and could lead to a reduction in S&P earnings of 10% or more. Political risk could also impact the Healthcare sector, although impacts are farther off. Technology continues to be an attractive sector, with investment in innovation expected to continue with demand supported by the pursuit of greater efficiencies and profitability in a lower-growth world. Macro Reports We’ve Read:Goldman Sachs Market OutlookMorgan Stanley Market OutlookUBS Market OutlookAlliance Berstein Market Outlook VC MacroThere were several significant conclusions from Cambridge Associates’ most recent report on the Venture asset class that resonated with us. At Fin VC our strategy and approach are closely aligned with the recommendations for Family Office and Institutional Investors made by Cambridge Associates and supported by other leading research on the asset class.Continuation of higher anticipated returns vs. Public Markets – “VC has generated compelling returns relative to public markets, both in recent years and over long-term time periods. Looking ahead, we believe the environment will continue to support attractive returns. Technological advancements, strong entrepreneurial talent, availability of capital, and fund manager skill are creating intriguing investment opportunities across multiple dimensions.”Fears of too much $ raised overblown in context – “When put into context, the amount of money raised in VC represents a fraction of the market value of the industries being disrupted by many venture-backed companies, and a fraction of the total addressable markets of emerging business categories being created by VC. VC at $340 billion net asset value (NAV) is less than 0.5% of the $85 trillion in global equity valuation.” Where we and others have concerns is in the broader Private Equity (growth, late, and buy-out) space where there is $800B+ of dry powder on the sidelines in North America alone (on a committed capital basis)Higher allocation to VC for Satellite Portfolio / Alpha gen – For Family Offices Cambridge “advocates to consider allocating 40% or more to private investments…with half of private investment allocations (20%) to VC…Factoring in the potential tax advantages of VC investing—such as returns being taxed primarily as long-term capital gain; opportunities to discount interests for gift, estate, and inheritance tax purposes; and possible qualified small business stock tax treatment—a 20% allocation can nicely position a portfolio for future generations.” We would note that Yale, who has out-performed peers by 2x over the past decade and is a bellwether for Asset Allocation strategy is targeting 21.5% allocation to venture and views the asset class as their top performer going forward.Emerging Managers continue to outperform – “new and developing fund managers (first two funds) consistently rank as some of the best performers” across vintages.Early Stage Managers will continue to outperform growth/late – “valuations for early-stage and growth sectors of venture have remained more reasonably balanced. For investors in the early and growth stages, increased funding options at later stages offer the opportunity for liquidity for early-round investors while allowing companies to remain private.”Value-added matters and loss ratios are narrowing: “VC funds are surrounding themselves with “incubator” forums and core communities of advisors, as well as setting aside capital for follow-on needs. These additional measures provide critical resources that enable start-up companies to find solid product market fit and to scale accordingly. This has had the dual effect of reducing return dispersion among managers and reducing the impairment and capital loss ratios of the underlying universe of companies. In the 1990s, the capital loss ratio was more than 50%. This has dropped significantly to about 20%…closer risk/return profile to global PE (buyouts and growth).”Returns reaped by VCs vs. Public Markets – “there looks to be a clear and sustainable trend of private markets replacing public markets. Over the past 20 years the number of publicly traded US equities has nearly halved, from 8,090 to 4,336. This compares to 8,352 unrealized and partially realized VC-backed companies in 2019. While not all these companies will survive, or prosper, many will generate significant returns for investors. As these companies stay private longer, the greater returns are increasingly reaped by early VC investors.” |

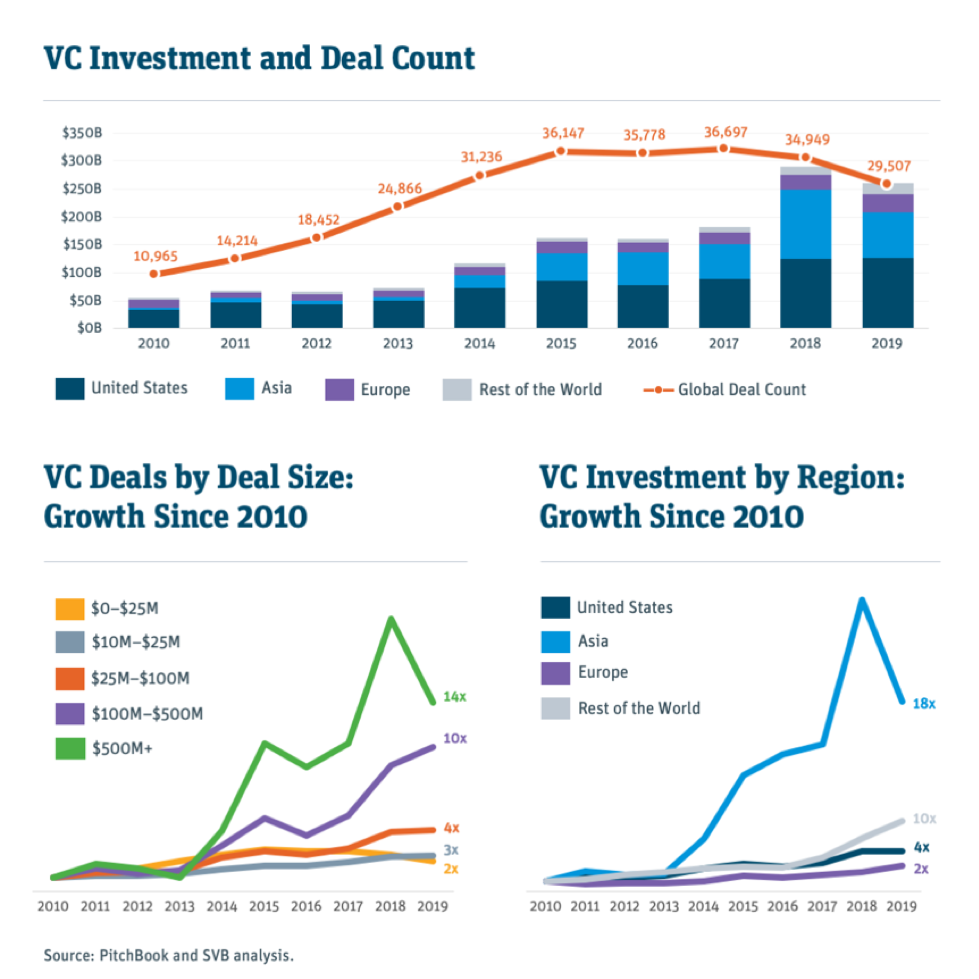

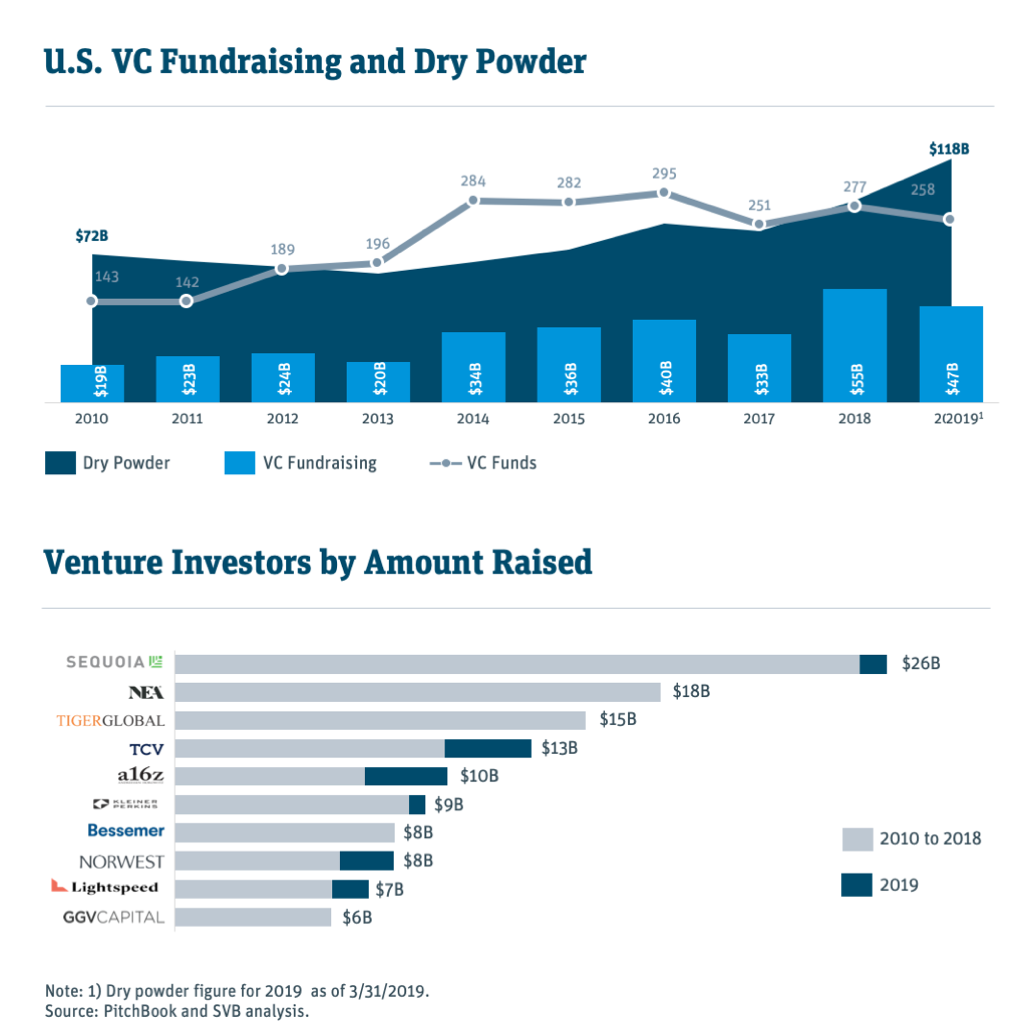

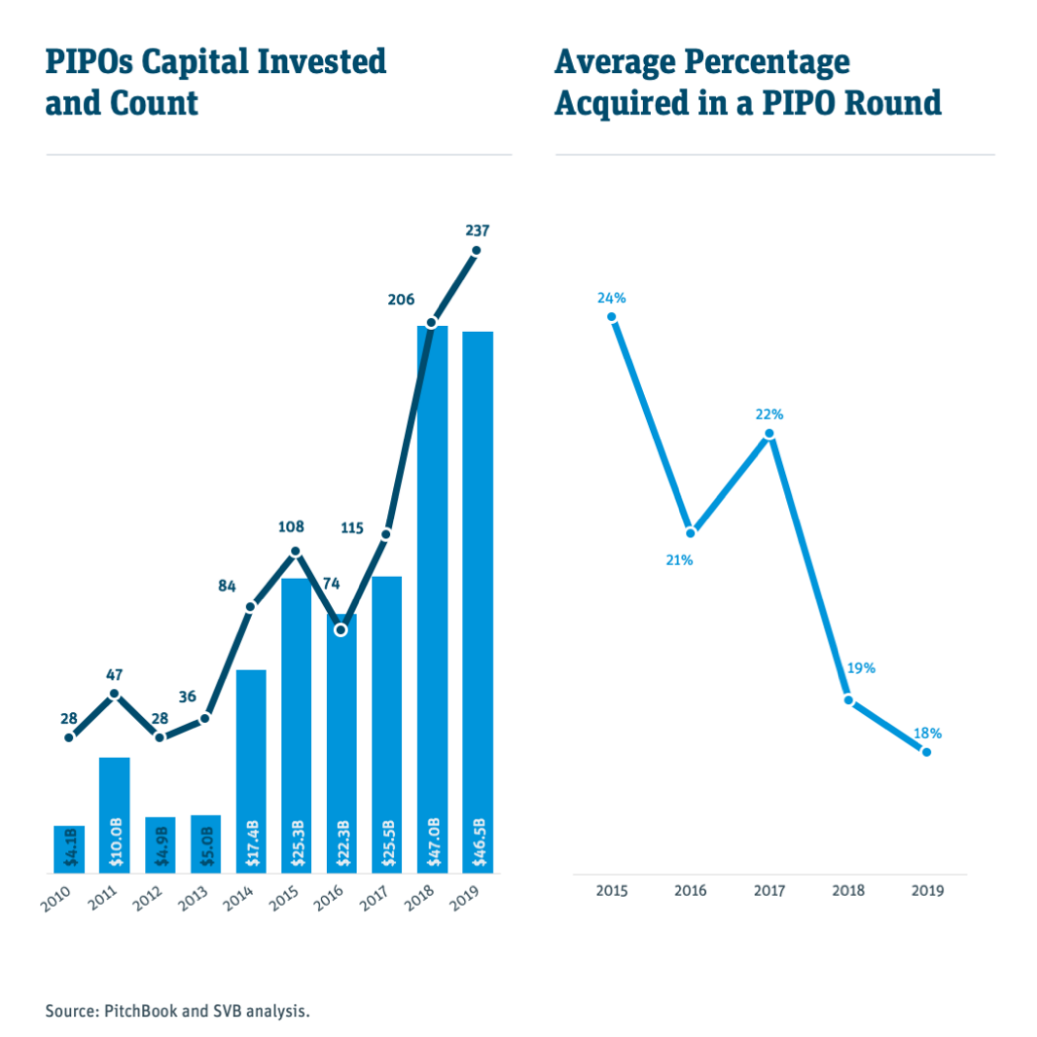

| The Micro Venture Capital MicroHeadlines: Global deal count continued its downward trend from 2017 at 29,507 in 2019 off of a total of 34,949 in 2018. Total financings were $250B in 2019, down from ~$300B in 2018 and the US dropped to 50% of those invested dollars. Indeed, global VC investment has grown 18x in Asia alone and “rest of world” has grown 10x in the last decade. By comparison, the US has grown 4x and Europe 2x over the same period. Deal sizing continued its upward trend with mega-rounds ($500M+) having grown 14X in the last decade and growth rounds ($100-500M+) up 10x over the same period. These “Private IPOs (PIPOs)” have risen 11x in the last decade, allowing companies to stay private longer, with 237 PIPOs in 2019 having raised $46.5B. However, these late stage rounds have become more competitive, driving up valuations, and thus ownership levels have dropped significantly from an average of 24% in 2015 to 18% in 2019. Conversely, smaller rounds ($0-25M), have only risen 2x, pointing to less competition and continued opportunity for out-performance for Early Stage managers.Why? Due to increasing fund sizes – driven by Softbank’s (overly?) aggressive late stage approach, accelerated re-ups, “tourist investors,” companies staying private longer, and the relative capital intensity of these companies, later round sizes and valuations have increased, particularly at the pre-IPO stage rounds. Remember, fund terms have not changed on average, you still have 5 year investment periods with 10 year fund lives (with 2-3 optional one year extensions), and thus with larger fund sizes and relatively flat team sizes, firms are forced to put more capital to work at the same investment pace. This has forced them to move into later/larger rounds, driving bigger checks, more competition, and higher valuations based on bidding dynamics rather than business fundamentals. Softbank’s governance and investment issues have been well covered and as a result Vision Fund II appears to be on pace to raise less than half of its $108B target, with $40B of it coming from Softbank itself. However, the knock-on effects on the rest of the PE/VC and LP community have not received sufficient coverage from our perspective. The above influences on the PE/VC community have driven cyclical investment issues which we have already seen born out in several poorly performing IPOs, and we believe there will be mean-reversion on fund sizing/re-up cycles and remain hopeful that Softbank will be more thoughtful in its second fund’s allocation (which should be helped by Elliot Management’s activist role). However, there are uncertain and potentially long term impacts to both Softbank’s LPs and the broader LP community. Given the increased exposure to VC/PE at this stage in the cycle and the lack of meaningful liquidity events we fear that the Endowment, Foundation, and Pension world could face allocation challenges going forward.LP commitments: US Venture firms raised $48B, lower than 2018 and SVB expects that fundraising will largely be flat in 2020, at between $40-50B. The number of funds has also fallen from 277 to 258 firms, with “mega funds” ($1B+) making up only 3% of funds raised but 30% of the capital. In total, US VC firms alone are sitting on $11B in dry powder, which is only a small fraction of the overall PE market.Liquidity: In the US, there were 159 IPOs in 2019, down from 192 in 2018 and ~500 during the peak in ’99 and ’00 (Statista). Additionally, there were 849 VC-backed M&A transactions, signaling a continuation of acquisitions as a strong exit option. There were 80 VC-backed IPOs in 2019, down 19.2% from 2018. The liquidity proceeds in 2019 trended higher, with gross capital raised totaling $28.9B, with a mean of $366M, the highest seen since 2012 when Facebook debuted. From an allocation perspective, as we have continually highlighted, Enterprise Software has continued to outperform broader TMT a trend that we believe will continue for years to come. To wit, per Renaissance Capital, 2019 saw nine enterprise SaaS IPOs, raising $11.2B and averaging 54% returns and the BVP Nasdaq Emerging Cloud Index, was up 41%.See below for charts/illustrations from our friends at SVB and Pitchbook in their “State of the Markets Report” |

|

|

|

| FinTech Micro Global 2019 FinTech Data – Courtesy of our friends at Pitchbook & FT PartnersFinancing Volume: $44.7 billion (Largest Financing: Paytm – $1.66 billion)InsureTech had the largest venture-backed growth, receiving $5B in funding, 60% greater than 2018Blockchain enabled companies continued to attract meaningful capital, at $1.4B, demonstrating that enterprise applications, like our portfolio company, Figure, are driving meaningful scale in Financial Services.# of Financing Deals: 1,814 (1,468 with announced $ amounts; 346 without)M&A Volume: $233.7 billion (Largest Deal: FIS Acquires Worldpay for $36 billion, followed by Fiserv’s $22B acquisition of First Data)# of M&A Deals: 982 (152 with announced $ amounts; 830 without)Global 2018 FinTech Data (updated):Financing Volume: $53.8 billion (Largest Financing: Ant Financial Raises $14 billion)# of Financing Deals: 1,652 (1,288 with announced $ amounts; 364 without)M&A Volume: $127.3 billion (Largest Deal: Blackstone Group Acquires Refinitiv for $20 billion)# of M&A Deals: 869 (184 with announced $ amounts; 685 without) |

| Firm UpdatesOur Unique Vision for VC: We believe the future of Venture Capital is “multi-strat” with deep industry sector expertise and a synergistic set of fund offerings including a Flagship offering principally US focused, Specialty funds that represent sub-strategies of the Flagship where we see significant greenfields, and Regional funds that focus on a specific geography and establish teams with deep local expertise and networks. Indeed, we deeply believe in specialization and a repeatable macro and thesis-driven approach to VC investing in which we proactively identify and source portfolio companies. Further, LPs desire less blind pool risk, want to understand what they’re investing in and in parallel, entrepreneurs want clarity on investment criteria, strategic alignment, and differentiated value-add. Hence, we have three funds we are operating out of presently and will continue to methodically and judiciously add to our disciplined approach. Alongside of our fund strategies, we believe LPs increasingly wish to invest directly in sponsored opportunities and have set up a co-investment platform, alongside of our funds (direct to cap table, no fee layer) and in Opportunistic special situations (growth/late stage that don’t align to our early stage strategies but around which we have conviction and unique access).Summary of Current Portfolio Companies: Notably across our ten companies we have been able to achieve diversification across our six sub-sector focus areas and geographically (US, Asia and EU), have multiple companies who have already raised subsequent rounds of financing, and our companies are powerfully diverse demographically, with three incredible female CEOs and rock star female/minority management teams. We believe strongly that diverse teams produce better outcomes and make superior decisions and will continue to actively support and seek diverse teams throughout our strategies. We are excited to continue actively working with all of our companies on business development, access to capital (equity/debt), global market entry, product roadmap strategy, and active recruiting. |

| Flagship Fund 1 |

(Alternative Lending) (Alternative Lending)SoFi is one of the leading FinTech platforms globally with an end-to-end set of product offerings across lending (student loans, personal loans, mortgages), banking (checking, savings, and debit), wealth management, and insurance (life). SoFi’s leadership team includes Anthony Noto (CEO), Michelle Gill (CFO), and Joanne Bradford (CMO). News | Talent Needs |

(Blockchain Enterprise Applications & Alternative Lending) (Blockchain Enterprise Applications & Alternative Lending)Figure’s vision is build an end-to-end financial services platform for consumers, enabled through web/mobile technology powered by AI, blockchain and other frontier technologies. Team includes Mike Cagney (CEO), June Ou (CTO), Alana Ackerson (CPO), and Cynthia Chen (CRO) and a management team including top industry/FinTech professionals. News | Talent Needs |

(Blockchain Enterprise) (Blockchain Enterprise)Coinsuper aligns to our Blockchain Enterprise Applications thesis, in providing an expansive set of services to the growing crypto-asset industry in Asia, with a focus on institutional investors. The company is based in Hong Kong and has a strong management and technical team, led by Karen Chen (CEO, fmr UBS Asia Exec) with deep financial services industry, FinTech, and blockchain/crypto experience. Further, the vision for the company aligns to our view on the role of exchanges and platforms in the space, in providing a diversified set of services primarily to institutional customers via multiple channels (Exchange, OTC, Brokerages, and Custodians). Our view is that Coinsuper will become the largest and dominant player in SEA and have an opportunity to be a top 3 platform in China and globally. News |

(InsureTech) (InsureTech)Avinew is solving for the auto insurance space broadly both B2C and B2B2C with a focus on semi-autonomous and autonomous driving. The team is partnering with affiliates, manufacturers, sharing economy companies and consumers to optimize insurance for the new age of auto. The team is led by repeat entrepreneurs and insurance experts, CEO Dan Peate (former CEO of Hixme), Ed Combs as Head of Product (one of the top auto insurance experts/underwriters globally), COO Jeremy Snyder (fmr Head of BD/Special Projects for Tesla), Randy Adams as CTO (fmr senior executive at Adobe, Yahoo, and HSN), and Steve Bentz as Head of Claims (30+ yrs experience across multiple insurance players). News |

(RE Tech) (RE Tech)CRE Simple provides an integrated end-to-end loan servicing platform that brings together an automated quote engine, intelligent task prioritization, collaborative workflows, and predictive outcomes. CRE simple focuses on the $1-10M loan market, which is a $200B market, of which the 20 brokers currently on the platform represent $30B of the market. Team is led by industry veteran Laura Millichap and repeat entrepreneur Brian Thompson. News | Talent Needs |

(RE Tech) (RE Tech)Nestio is the leading leasing and marketing platform for multi-family, enabling owners and managers to generate more profits, efficiency, and analytical insights across their portfolio. The team is led by Caren Maio (CEO), Mike O’Toole (CTO), Tyler Christiansen (CRO), Scott Wolfgang (COO), and Ben Rubin (VP of Product). The team has built strong traction with real estate property managers, landlords, and brokers, driving strong stickiness with a growing customer base. News | Talent Needs |

(Asset Management) (Asset Management)Aiera is headquartered in New York and is led by CEO, Ken Sena (formerly global head of internet equity research at Wells Fargo and held senior positions at Credit Suisse, Bear Sterns, and Salomon Smith Barney) and President/CRO, Chad Doerge (formerly held senior roles at Tomahawk, Evercore ISI, and Deutsche Bank). Aiera is an adaptive deep learning platform design to enhance active fundamental investment strategies, generally Buy/Sell/Hold calls (long and short recommendations) and clear, human-readable thesis summarizations using a proprietary neural interrogation tool and advanced linguistics techniques. News |

(Enabling Tech) (Enabling Tech)Netomi has built an advanced AI/ML deep learning platform to address the challenges of customer service across all industries, but with massive implications for Financial Services. Companies spend ~$400B/yr on customer services agents alone with over 1B tickets being generated a day via phone, e-mail, and live chat. The team is tackling this problem with a platform that provides enterprise customers a seamless way to automate customer service interactions across e-mail, chat, and social. The team is led by Puneet Mehta (CEO) and includes notable advisors like Dick Costolo, Demis Hassabis (DeepMind), and Nikesh Arora (PA Networks). News |

(Blockchain) (Blockchain)BrainTrust is “building a fair future for work” connecting global companies and knowledge workers on a dynamic talent platform powered by Blockchain/DLT. The platform supports employers in sourcing top tech freelancer talent, who have a central place to aggregate work history/reputation, create transparency and tracking in projects, manage teams, and receive tokenized payments. The token (BTRUST) is the sole ownership unit and provides incentive alignment and network effects for referrals, while increasing value from Gross Service Volume (GSV) from employers. The team is led by seasoned repeat entrepreneurs, Adam Jackson, Brian Flynn, and Gabriel Luna-Ostaseski. News | Talent Needs |

(Asset Management) (Asset Management)Numbrs has built the future of asset management and digital banking. Building its platform out of Switzerland, the team has scaled principally via a B2B2C model to offer full stack financial services through bank, asset management and insurance partners across the EU. The product utilizes deep AI/ML, data aggregation, behavioral analysis, and open APIs. The team is led by Martin Saidler (CEO), Christina Rogge (Ops), and Severin Ruegger (CSO). Other investors include the Investment Corp of Dubai and global FOs such as Marcel Ospel, Sir Ronald Cohen, and Sir Victor Blank. News | Talent Needs |

| Co-Investment Platform |

(Asset Management) (Asset Management)Tradeshift (TS) is the world’s largest, open, digital commerce platform enabling enterprises to connect, transact and collaborate with all of their business partners. The management team is led by founder and CEO Christian Laang and the company maintains a long and global perspective on their platform and future, incorporating frontier tech like blockchain, AI/ML, and IoT. News | Talent Needs |

(Enabling Technology) (Enabling Technology)Onfido is the leader in digital ID, providing 3 layers of verification – government issued ID, biometric scan, and voice patterning/recognition. Companies like Square, Revolut, BBVA, Uber, Google, and Avis use the Onfido API to mitigate fraud/regulatory risk, manage hiring diligence, expedite KYC/AML requirements, and conduct ongoing cybersecurity checks on customer and employee access. Onfido is a team of 195 across NYC, SF and London. News | Talent Needs |

(Alternative Lending) (Alternative Lending)DailyPay is modernizing payroll through FinTech, providing a thin layer between legacy payroll, time management systems, and HR systems to enable employers to deliver financial services to their employees, with short term lending being the starting point to a more comprehensive product roadmap. DailyPay is generating a double bottom line impact by combating the punitive pay-day lending business and offering hourly workers, freelancers, and independent workers an alternative to taking advances on future earnings – reducing financial stress, turnover and costs to both employees/employers. DailyPay earns revenue by charging employees a fee each time they request an advance on their payroll. The company caters primarily to hourly workers, earning $20-50K/year, who require short term advances to handle household expenses. The fee is a one-time transaction fee and does not depend on amount or length of time to payday. In this way, the fee resembles an ATM fee which users understand and view as transparent. News | Talent Needs |

| Warm regards, Fin VC Team |